Owner wants to develop business further

Key Highlights

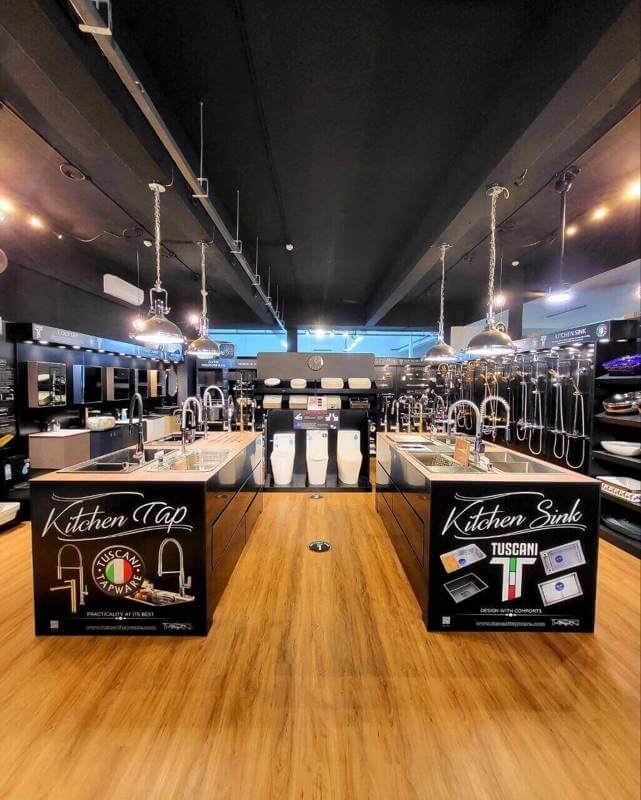

Bathroom and kitchen solutions business founded in 2004 with over 20 years of operating history. Supplies bathroom and kitchen products to residential developments, retailers, contractors, interior designers, architects, exporters, and homeowners. Sales channels include retail distribution, project/contractor sales, specification via designers and architects, export sales, and direct-to-consumer e-commerce. E-commerce presence includes Shopify, Lazada, and Shopee. The business holds three registered trademarks with IPOS. Team size is stated as 6–10, operating with a physical showroom model.

What Makes This Business Unique

The business combines a long operating history (since 2004) with formal intellectual property protection through three IPOS-registered trademarks. It operates as a multi-channel platform spanning retail distribution, project-based sales, professional specification (designers and architects), export activity, and direct-to-consumer e-commerce on Shopify, Lazada, and Shopee. A physical showroom is positioned as a customer experience center supporting both homeowner and trade engagement. The product range spans bathroom products and kitchen mixers/accessories, covering both mass-market and premium segments.

Operations

Revenue is described as mostly one-off transactions, driven by product supply across retail, project, and direct-to-consumer channels. Operations include sourcing and manufacturing relationships in China, with stated procurement and quality-control systems. The business runs a physical showroom and sells online via Shopify, Lazada, and Shopee. The portfolio includes designer bathroom products, kitchen mixers and accessories, and project-based solutions. The business structure is stated as a sole proprietorship with a team size of 6–10.

Customers & Market

Customer types include residential developments, retailers, contractors, interior designers, architects, exporters, and homeowners. Sales are generated through a mix of retail distribution, contractor/project sales, professional specification, export market activity, and direct-to-consumer online channels. Products are positioned for both mass-market and premium segments across bathroom and kitchen categories.

Why This Business

Operating history since 2004 provides an established platform and market presence that typically takes years to build. Three registered IPOS trademarks provide transferable brand-related assets that a new entrant would need time and cost to replicate. The buyer inherits an operating multi-channel sales setup across retail, projects, specification-driven sales, export activity, and established e-commerce channels (Shopify, Lazada, Shopee). A physical showroom provides an existing offline sales and brand-experience asset that would require capital and setup time to recreate.

| Year | Revenue (SGD) | Earnings (SDE) | NET MARGIN |

|---|---|---|---|

| 2025 | SGD 1M | SGD 300K | 30.0% |

Real estate: S$300,000

Trademarks & Branding: S$50,000

N/A

AI paraphrased description: This SWOT analysis helps you quickly see the good and bad sides of a business, plus the opportunities to grow it and the risks to watch out for. It makes it easier for buyers to decide if a business is worth buying without getting lost in complicated details

Google rating is 4.6 across 58 reviews, which is a decision-grade volume for a customer-facing showroom retailer in Singapore (sub-15 review profiles are typically not reliable signals).

This level of social proof can reduce buyer CAC in the first year post-acquisition compared with a new entrant that must build reviews and visibility from zero.

Seller-submitted 2025 figures indicate SGD 1.0M revenue and SGD 300k SDE (~30% margin).

For Singapore fittings/retail-wholesale operators, net margins are often ~5–15% (directional). If verified through P&L and bank flows, this profitability would support valuation and provide headroom for a buyer to invest in growth without immediately compressing returns.

The business is positioned to sell through a showroom plus trade/project channels (contractors, residential developments), spec-in via designers/architects, and online channels (website and marketplaces).

In Singapore, many small operators are either purely showroom retail or purely trade supply; having both can diversify demand, provided pricing and channel conflict are managed.

Seller-reported: three IPOS-registered trademarks are included as intangible assets (stated value SGD 50k).

In Singapore home-improvement retail, branded fixtures and identifiable collections can support premium positioning versus generic importers, but a buyer should confirm the marks are registered to the selling entity and are assignable with the transaction.

The operation includes a physical showroom and a web storefront with product merchandising, which reduces the time and capex needed to launch a comparable consumer-facing fittings business.

Seller-reported tangible assets include a showroom/real estate value of SGD 300k; for Singapore SMEs, acquiring an existing fitted-out showroom can be materially cheaper than building a new one, subject to lease/title verification.

The seller states the business structure is a sole proprietorship, while third-party corporate directory listings reference an incorporated entity (UEN 201832082D) with incorporation in 2018.

In Singapore, a sole proprietorship sale is typically an asset purchase (not share sale), which changes how licences, staff, contracts, IP, and platform accounts transfer. A buyer should confirm the exact selling entity and what is being acquired (assets vs shares) through ACRA BizFile records.

The revenue model is described as mostly one-off transactions, which is common in renovation-linked categories but typically produces less predictable monthly cashflow than contract supply agreements.

For Singapore SMEs, businesses with recurring/contracted revenue (e.g., term supply to renovation firms or maintenance/replacement programs) generally command higher valuation multiples due to visibility; the current model may require a buyer to maintain active lead generation to sustain sales.

Only 2025 revenue and SDE are provided; there is no multi-year trend, no gross margin view, and no working-capital detail (inventory levels, aged payables/receivables).

In Singapore retail/wholesale, inventory and project receivables can materially change true cash generation versus accounting profit, so valuation requires at least 2–3 years of financial statements and bank reconciliation.

The showroom is in an industrial complex rather than a mall or high-footfall retail corridor, which generally reduces impulse walk-ins for consumer-facing fittings purchases.

For Singapore showroom retail, this usually shifts the mix toward appointment-driven visits (designers/contractors) and digital lead capture; a buyer should budget for sustained marketing and trade relationship management rather than relying on location foot traffic.

The seller reports selling via Lazada and Shopee in addition to the website; third-party search results also show live marketplace storefronts.

For Singapore e-commerce sellers, marketplace fees, ad costs, rating rules, and search algorithm shifts can compress margins; without channel revenue breakdown, a buyer cannot assess how exposed the business is to platform policy changes.

Within 6–12 months, a new owner could formalise contractor/designer sales into tiered supply agreements (rebate tiers, fixed-price bundles for common renovation packages, priority delivery) to reduce the one-off nature of revenue.

This is achievable using existing channels (showroom + trade clients) if the customer list, historical purchase patterns, and product margin by category are documented first.

Over the first 90–180 days, the business can package downloadable spec sheets/BIM-style product data, finish sample request flows, and designer partner terms to increase the probability of being specified into projects.

This leverages the current showroom and product catalog, but requires prerequisite work to standardise SKUs, lead times, and warranty terms to reduce friction for specifiers.

Within 3–6 months, the website can be optimised around high-intent categories (showers, mixers, accessories) with clearer installation compatibility guidance, comparison tables, and enquiry/WhatsApp flows for higher-ticket items that customers often research before visiting a showroom.

This is realistic because the site is already live; the prerequisite is measuring current funnel performance (GA4, ad account data) and identifying the top 20 SKUs driving revenue and returns.

In 6–9 months, a buyer can operationalise Google review strength into referrals by implementing post-installation review requests, designer referral incentives, and case-study content that ties back to showroom appointments.

This is achievable because the business already has 58 Google reviews; the prerequisite is mapping the customer journey (purchase → delivery/installation → follow-up) so the review ask is consistent and compliant.

Sales tied to home renovation cycles (HDB/condo turnover and discretionary upgrades) can soften when household budgets tighten or renovation volumes slow, impacting both showroom and online conversion.

Because the business is described as mostly one-off transactions, it is more exposed to demand swings than operators with contracted supply or maintenance-based repeat orders.

If Lazada/Shopee contribute a material share of sales, rising ad bids, commission structures, and stricter fulfilment KPIs can reduce unit economics even if order volume holds.

This is particularly relevant for bulky/fragile bathroom products where shipping/returns are costlier in Singapore, and where price comparison is direct within marketplaces.

Seller-reported operations include sourcing/manufacturing relationships in China; shifts in freight costs, lead times, FX, or supplier MOQ terms can tighten margins and create stock-out risk.

For a showroom-led model, inconsistent availability can directly reduce close rates (customers substitute brands quickly), so supply resilience is a key external risk to performance.

Singapore has multiple established sanitaryware and home-improvement chains and large specialist showrooms that can compete aggressively on bundle pricing, financing, and installation partnerships.

Given this business’s small-team scale (seller reports 6–10 staff), matching chain-level promotions and logistics may be difficult without sacrificing margin, making differentiation via spec-in relationships and curated ассортимент important.

DATA DISCLOSURE

Please wait while we prepare your results